It appears that the US have been critical of Germany's attitude towards exports. Basically, the US, now backed by the IMF, are critical of the German Chancellor's claim that exports indicate a healthy economy. Although I disagree with Merkel's claim for the pure reason that an export-based economy is basically relying on others to prosper, I cannot help but cast my doubts on the stance many have taken against Germany.

My regular readers will certainly know that I am not a friend of German policy on most subjects. Still, I find it rather odd that a country which is having trouble with too much imports and is actually trying to decrease its current account deficit is trying to support that another country shouldn't have a large current account surplus. To be honest, I find it rather hypocritical, especially from the IMF's point of view. The fund’s First Deputy Managing

Director David Lipton urged Germany to "lift its sights to the global

horizon" and that cutting excessive deficits in the euro area

“simply can’t happen unless surpluses are down as well.”

Maybe Lipton is right and maybe Merkel should pay attention to what he is saying. Still, what was his employer doing when they organized the bail-out of 5 Eurozone countries in past 5 years? Simply, they were creating the situation that Germany is currently "exploiting": high uncertainty, low competitiveness, high unemployment and most importantly a depreciated euro. I will not delve into whether Germany had a say in all those or not; it is irrelevant to the role the IMF played. The IMF is supposedly an independent organization which assists ailing nations with or without the assistance of others. In any case, the IMF has supposedly been independent and unbiased in both its estimations and its opinions.

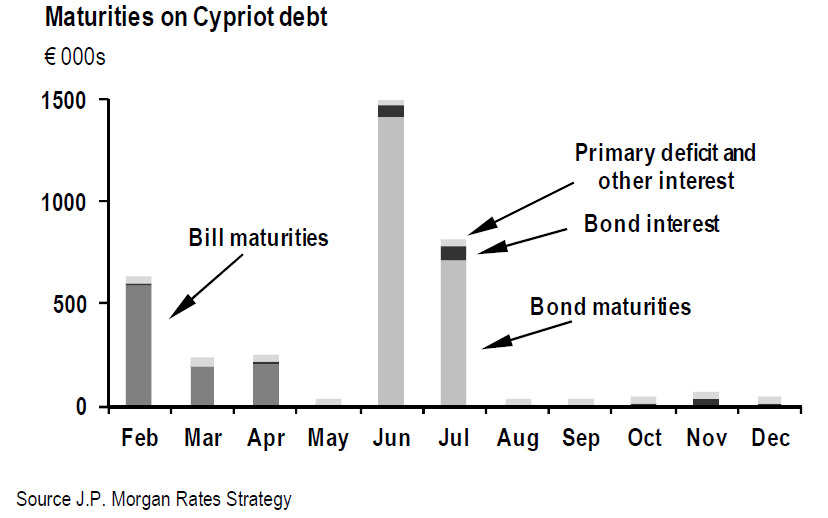

Yet, where was this opinion when the Irish bail-out was orchestrated? Or how about the Spanish or Portuguese or Greek or Cypriot one? Did the IMF change its stance on the subject as time passed on? This is an article from last February commenting on what the Washington Post published as Olivier Blanchard's mea culpa on the IMF policies in Greece. Yet, the directors never changed their tune and did the same in Cyprus just a month later. Now, they are basically blaming Germany for taking advantage of a situation they have created. But is it just Germany though or is it a general trend in the Eurozone surplus? Eurostat data favour the latter view: Euro-Area trade surplus increased to 7.1 billion in August 2013, compared to 4.6 billion in August 2012 (which was not just because of the North surpluses).

There are those of course who are not taking a like to the US stance on the subject. FT's Gideon Rachman comments "If you had to single out a major Western economy whose irresponsible

economic policy has posed a persistent danger to the global economy, the

obvious candidate would be the United States." His points are correct all the way. The Great Recession alone supports his view, and if we wanted we could easily find more (the Great Depression for example). QE has been a drag on both the US and the world economy for long now and stories about whether the Fed should taper or not (or whether it can) are a major cause of uncertainty, without the officials doing anything about it. In addition, if we are to pin-point, why just Germany? China and Japan have been doing the same for years yet there has been no

criticism of their actions (other than the one for the remnibi's

"constant" depreciation).

Others though still think that Germany is, in their words, "a weight on the world". The arguments Wolf makes are correct and the risk of permanent deflation exists in the periphery. I doubt whether such a scenario would occur in reality, yet I think the probability exists and deflation in 2014 is something we can expect. Is Germany employing a beggar-thy-neighbour policy? To be honest, I doubt whether it can. Germany can earn significant amounts from exporting heavily, yet this comes at a cost: inflation in Germany as current data show is at 1.7% thus far, slightly higher than the EA average of 1.6%.

Is this increase significant? Perhaps not, but the inflation monster so feared by Germany might prove too hard to kill given the ECB rate cut and the increased probability that the rest of the Eurozone recovers. As Evans-Pritchard puts it, the ECB is ready to print and Germany is ready to scream; he also rightly points out that a bout of deflation in Italy is much more severe than a bout of inflation in Germany. My take is that the ECB will finally move the way it should. Although the rate cut was much ado over (almost) nothing, it was a step towards the right direction, mainly to boost inflation in Germany and the North and investment and consumption everywhere else.

In any case, arguments like "the Germans do not work as hard as they think" (which Matt Yglesias makes) are really unnecessary and I remember deconstructing them more than a year ago. The US exports as much as Germany Matt states, but forgets to mention that the former's GDP is more than 4 times larger than the latter's and its population approximately 4 times as much, meaning that imports will be (and are) much higher and the current account will be negative. Yet, that is not a problem for the US since it has a sovereign currency of its own. Germany and the rest of the Eurozone do not. As he again points out the proposal is one to "buy more foreign-made goods and services." But these all depend on their cost and how they fare with German products. And let's face it: German products are (usually) of great quality.

Thus, as deflation sets in the rest of the Eurozone in 2014, prices in Germany will rise as a result of exports, making goods from other Eurozone countries look more appealing. This will help both the periphery countries increase their exports and Germany reduce it's dependence on foreigners (i.e. reduce exports) with the additional effect of appreciating the euro. The bottom line is that high exports are not a sign of a healthy economy, they are a sign of dependence on foreign factors. Still, blaming a country for high exports when you cannot control your own or when you were at large the culprit for the creating of the situation which allows them to pursue such policies does not make sense at all.

.png)