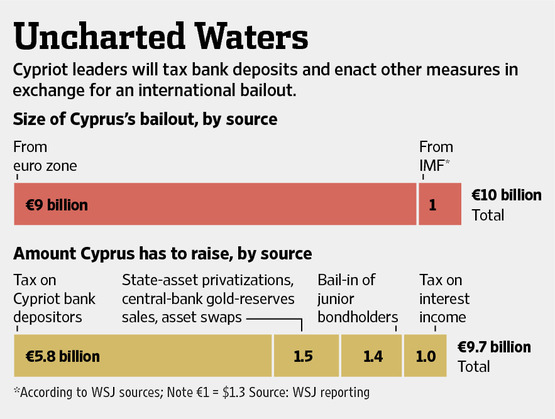

For those who haven't heard, the latest Eurogroup summit on Friday (or better Saturday morning) ended with an agreement for Cyprus to impose a one-off deposit tax of 6.75% on deposits up to €100,000 and 9.9% for over that amount. In addition, the Cypriot government has agreed to increase company tax to 12.5% from 10% and privatize some of its profitable state-owned businesses. The total amount expected to be generated from the Cyprus deal is the following:

|

| Source: Wall Street Journal |

The so called Troika has been arguing that a €17bn package would be sufficient to revive the island's economy, yet it would make its debt burden unsustainable as it approximately equals Cyprus's GDP. Yet, it appears that the total funds which have to be generated will near €20bn, of which €5.8bn will be produced via the deposits levy. A levy which has caused global outrage given that it affects deposits which were considered to safe under every scenario; most importantly it creates a precedent which experts fear that can be used against Italy or Spain when they opt for a bail-out. Another question which has not been answered yet is why was the amount increased and if the Eurogroup is essentially forcing Cyprus to pay on its own.

The German Chancellor Angela Merkel, as well as most German politicians who appear to support the aforementioned deal, stated that Cypriot depositors should assume responsibility for what their banks have done. Money-laundering and the extreme size of the Cypriot banking sector are often brought forward as the rationale behind their actions. (for a review of the money laundering issues in Cyprus, Matina Stevis's article in Wall Street Journal is an excellent source)

Let's take these issues from the start:

1. Money-laundering: It may (or may not) be true that Cypriot banks have been involved in money laundering activities. However, it is quite unlikely that ordinary people who are working in 9-5 jobs in any sector are involved in this. Yet, it is these people who are being targeted in the levy. Not high-profile managers, lawyers or bankers but people who are struggling to save some money to pay for their children's education or have an easy retirement.

2. Risk Premia: Some have also argued that "with interest rates as high as 5% in term deposits there was a substantial risk premium which indicated danger". Perhaps this is true. However, these rates only apply for term deposits with amounts in excess of €50,000 and not for current accounts or savings accounts where most of the money lies. In addition, not everyone is a hedge-fund manager with the ability of sending enormous amounts of money abroad. Everyday citizens cannot afford the luxury of having their paycheck deposited in Germany or anywhere else in Europe for that matter.

3. The size of the banking sector: Stories have been circulating the web that the problem is Cyprus's enormous banking sector. The following graph indicates that private sector deposits in Italy are much higher than the ones in Cyprus. From the same data it appears that Ireland's case was much worse prior to 2010. No-one can doubt that the banking sector is big indeed. Yet, forcing it to break-up (for example exiting from Europe) will mean that you are depriving it of many growth opportunities over the next decade; especially after it has taken all the losses from bad loans and bond haircuts.

4. Greek PSI: One cannot help but wonder why the EU had not taken into consideration that the cause of the Cyprus problem was essentially the decision to slash the Private Sector Involvement in Greek bonds by 70% (a proposal that the former Cyprus Central Bank Governor Athanasios Orphanides had strongly opposed). The decision cost Cyprus approximately €5 billion (without counting for the bad loans which arose as a consequence).

The worst part of the deal is that it is bound to set a precedent: if Italy applies for a bail-out fears of deposit haircuts will wreck havoc in the country's economy with a bank run bound to occur as soon as the news hit the market. Although Cyprus is not systemic per se, the trust issues which arise are. From now on, every time a country will opt for a bail-out fears of deposit haircuts will evoke memories of the Cyprus case.

Frances Coppola wonders "under what type of taxation scheme are people provided with shares to compensate them for the taxes they have paid?", while on another post yours truly has argued against risk-free assets transforming to risk bearing ones. While the Cypriot Parliament will reconvene tomorrow the question on when the banks will resume business is still vague: Although today is an established bank holiday, tomorrow has been announced as one as well. New information says that a new plan will involve less cuts for those under €100,000 (approximately 3%), yet this is still unofficial. In addition, small depositors are almost sure not to take their money abroad. It is the big depositors, with millions of funds who are the threat to the island's banking sector.

What poses the greatest threat for Eurozone's health is not that Cyprus will cause a bank run in other Member-States; it is highly unlikely (although a run will probably occur in Cyprus, with foreign depositors leaving en masse from the island). What is feared is the precedent: if they have done it before, they can do it again. And an escalating crisis arising from bank runs in Italy or Spain under rumours of bail-out could probably bring the Eurozone at its knees.

No comments:

Post a Comment