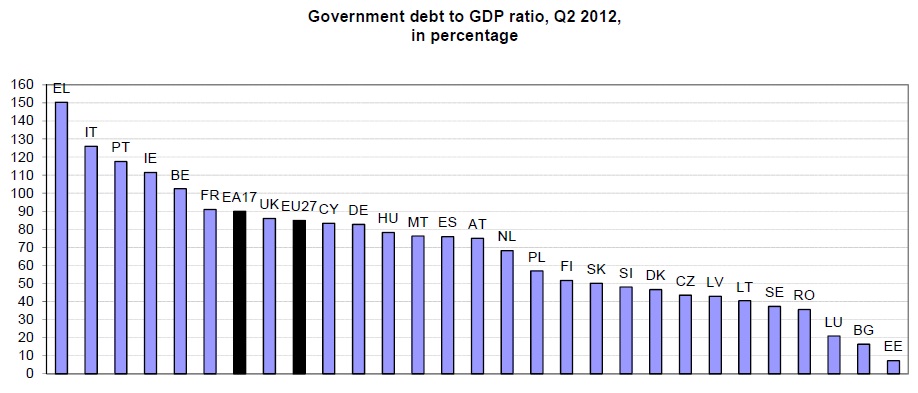

Nothing unusual about yesterday's announcement by Eurostat: Government debt in the EA17 and the EU27 in 2012's second quarter rose by 1.8% and 1.4% respectively. The usual suspects came up first with Greece reaching 150.3%, Italy 126.1%, Portugal 117.5% and Ireland 111.5%. Twenty out of a total of 27 Member-States have increased their debt burden over the last quarter.

|

| Source: Eurostat |

The next two candidates for a bail-out

memorandum, Cyprus and Spain, have seen their debt reach 83.3% and 76% of GDP

respectively. If Cyprus can negotiate the terms with Spain, then the

terms might not be so rough on the island. If left alone, fear for the

worst. Spain on the other hand, does have an ace up her sleeve. With

debt reaching "just" 76% of GDP, the nation can negotiate for a lighter

memorandum which would allow her not to impose extreme austerity

measures to an already shaking economy. For those interested, debt in Spain rose by 9.3% on a yearly basis, and in Cyprus by a staggering 16.5%. A reminder: those who believe that the over-spending South is the cause for the recent crisis should look at the announcement and note that Spanish debt was just 66.7% in 2011 and Cyprus's 66.8%, much lower than France's, Germany's or the UK's at the time. (actually both countries' debt is still lower than the aforementioned three, with Cyprus just having a 0.1% larger debt than Germany)

Another question is what is going to happen with Italy. Although Mario Monti's measures have managed to keep the debt increase to 2.4%, if the country's debt does not begin to fall soon then they might face greater troubles than they expected. In a yearly basis, from 2011Q2 to 2012Q2 Italy's debt has increased by 4.4%, which is not good news at all.

For some good news, the IMF has approved a €1.5 billion loan disbursement to Portugal today, confirming that the nation is on track with its €78 billion international bailout. Nemat Shafik, deputy managing director of the IMF has stated that: "A weaker external outlook and rising unemployment have increased

risks to the attainment of program objectives. Additional

efforts are necessary, with the support of euro-area partners, to

further advance fiscal consolidation and boost long-term growth."

Let's hope that they keep that "long-term growth" goal in mind and at the same time remember that for long-term growth, the short-term one is also needed.

No comments:

Post a Comment